Kathy Lafayette shares a home with her mother, Emma Titus, in Grass Valley in the Sierra foothills. They spent $3,000 clearing their property of trees and brush but still lost their homeowners insurance. (Mary Franklin Harvin/KQED)

After more than three decades in the Sierra foothills town of Grass Valley, Emma Titus lost her homeowners insurance last week. Her insurer, The Hartford, said she hadn’t done enough to fireproof her property, a 5-acre spread with old-growth pines and fruit trees.

“Never missed a payment. Never had a claim. And all of a sudden they can’t insure me,” said Titus, who said her house had been covered by The Hartford for 35 years.

Before the nonrenewal notice came, an inspector from The Hartford visited Titus’ property and gave her three weeks to clear it. But with all the brush, trees, an old grapevine and more, there just wasn’t enough time, she said.

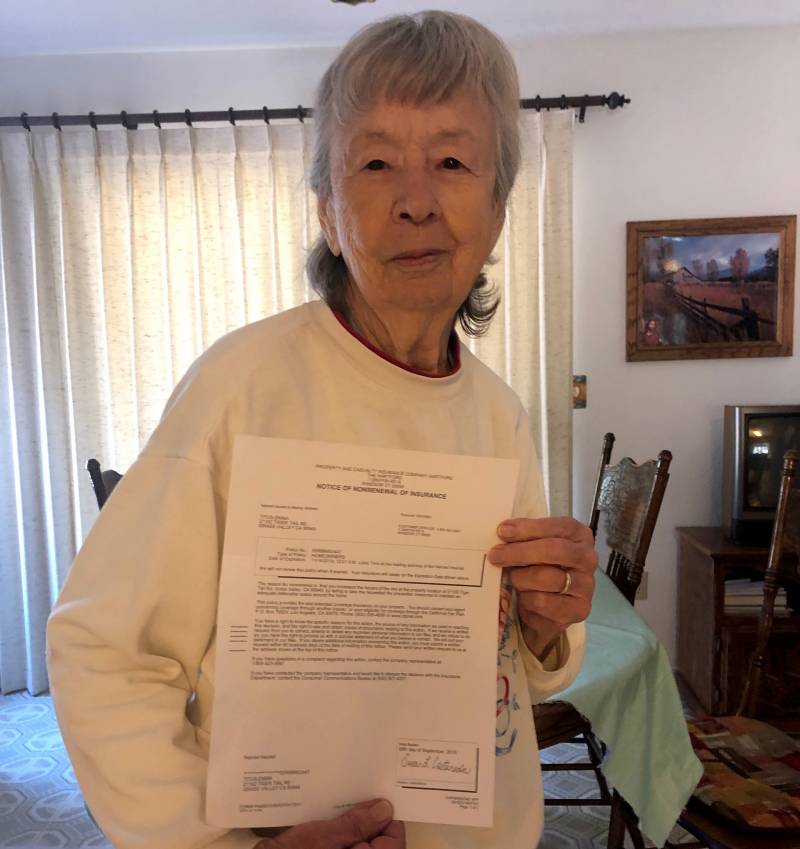

Emma Titus holds a letter of nonrenewal from her insurer, The Hartford. Her homeowners policy expired Nov. 14, 2019. (Mary Franklin Harvin/KQED)

Still, even after the three-week deadline had passed, Titus continued to clear her land. In October, she sent her insurance company photos documenting the mitigation work she’d done and receipts for the clearing costs, which she said totaled around $3,000. She hoped that she would earn reconsideration, but on Nov. 14 her policy expired anyway.

Titus said she thinks The Hartford doesn’t really care how fireproof her land is — she thinks they just want out of California.

Sponsored

“California’s been declared a fire hazard state, and that’s the reason,” she said.

Simply Denied

When Titus and her late husband bought a plot of land to build on in the early ’80s, no one ever discussed fire risk, she said.

“At that time, they wouldn’t let us cut trees down,” she said. “They marked one tree that we could cut down … to build this house.”

Emma Titus waters bushes in her front yard in Grass Valley. She said she spent $3,000 on clearing her land to make her property more fireproof. (Mary Franklin Harvin/KQED)

Since the Camp Fire devastated the town of Paradise last year, Titus has noticed a dramatic uptick in concern about fire risk from home insurers and other residents.

“They didn’t have a route to get safely out of [Paradise]. We don’t either. And they weren’t thinking about that when they built Grass Valley,” said Titus’ daughter, Kathy Lafayette, who lives with her.

When insurance companies assess homes for renewal and premiums, they assign risk scores to properties. Risk factors can include a home’s proximity to water sources, the amount of dry brush on the property that could fuel a fire and the local topography.

Many homes in Grass Valley and much of Nevada County are like Titus’: perched at the end of windy narrow roads, far from fire departments and water sources. Cal Fire has labeled Grass Valley a “Very High Fire Hazard Severity Zone,” and designated it as one of its 35 Priority Projects.

Nevada County District Supervisor Ed Scofield, who was born in Grass Valley, said he’s noticed a recurring theme of complaints from constituents like Titus. He said many residents feel like they’re being strung along by insurers that have no intention of renewing their policies, even after owners install fireproofing systems like irrigation.

“I know of property owners that have done major mitigations to even having their own fire systems on the ground … that are simply denied,” Scofield said.

Jeff Pettitt, head of Nevada County’s Office of Emergency Services, has heard similar complaints from residents.

“They’ve put out all this money to make their home defensible per their insurance company and they still get canceled,” he said. “That’s got to be an incredible frustration for them.”

But the fact remains that insurance companies have no obligation to factor homeowners’ efforts into their renewal or premium rate-setting decisions.

“California has … no mandate that insurers give you any credit for spending money to make your home more resistant to damage or reward you or give you a break or even keep you as a customer,” said Amy Bach, executive director of the consumer advocacy group United Policyholders.

‘I’m on my own’

In August, state Insurance Commissioner Ricardo Lara hosted a fire insurance town hall in Grass Valley. So many homeowners flooded the venue that they spilled out into the parking lot and, according to Supervisor Scofield, also crowded into a remote location. Several thousand people watched live streams online.

Titus’ daughter, Lafayette, was there, but said the forum left her feeling like homeowners are in this fight alone.

“I’m on my own. Now I have to do what I need to do to take care of myself and my family and try to be as safe and prepared as possible,” Lafayette said.

Many Nevada County residents are forming their own support networks. They’ve created fireproofing programs through the California Fire Safe Council, which has given more than $100 million in grants over the last 15 years for creating defensible space and education projects.

Some communities have also established their own local awareness groups through the National Fire Protection Association’s Firewise Communities program, which provides information on how neighbors can organize to protect their homes together.

“I think we have more Firewise Communities in the county than any other county in the state,” Scofield said.

The county seat, Nevada City, even launched a prescriptive grazing campaign, or as they called it, “Goat Fund Me,” to raise enough money to deploy goats to eliminate overgrowth by grazing city-owned land.

Nevada City’s “Goat Fund Me” campaign raised money for goats to graze and clear overgrown lands. (Courtesy of Reinette Senum)

But what about all the folks stuck struggling with astronomical premiums or who have mortgages and can’t forgo homeowners insurance?

United Policyholders’ Bach says there’s a precedent of state governments stepping in with legislative policy to protect insurance policyholders who can’t get dependable or affordable coverage.

“Many other states have had to put those mandates into place because insurers wouldn’t come to the table willingly,” Bach said.

Michael Soller, deputy commissioner of communications at the state Department of Insurance, agreed.

“Absolutely there’s a role here for the state,” he said, adding that his department wants to see more transparency from insurers about how they assess risk scores.

If a homeowner is doing work to mitigate their property, “it should be reflected in [their] risk score,” Soller said.

In the meantime, Titus is looking for coverage she can afford. The only quote she’s gotten so far would cost her over $7,000 a year — more than $5,000 more than what she was paying before her policy was canceled.

lower waypoint

Stay in touch. Sign up for our daily newsletter.

To learn more about how we use your information, please read our privacy policy.